1) Step 1- Problem or Opportunity Statement

In previous posts (W13 and W14), we have mentioned processes map for estimating and budgeting that owners can use as a guide to calculate the optimum cost estimate for developing future assets.

It was missing an analysis to determine what processes are equivalent between each other and identify if all of the alternatives have most of the processes required to produce an optimum outcome.

In addition, we can assess if we can combine them and get a more complete process for estimating and budgeting.

2) Step 2 – Feasible Alternatives

We have chosen the following entities:

- AACE International: Cost Estimating and Budgeting Process Map from Total Cost Management Framework

- Guild of Project Controls: Overall Cost Estimating and Budgeting Process Map

- Government Accountability Office: Cost Estimating Process

- American Society of Professional Estimators: Standard of Practice

- Project Management Institute: Project Management Body of Knowledge – Project Cost Management

3) Step 3- Develop the outcomes for each alternative

Total Cost Management from AACE International suggests the following Process for Cost Estimating and Budgeting:

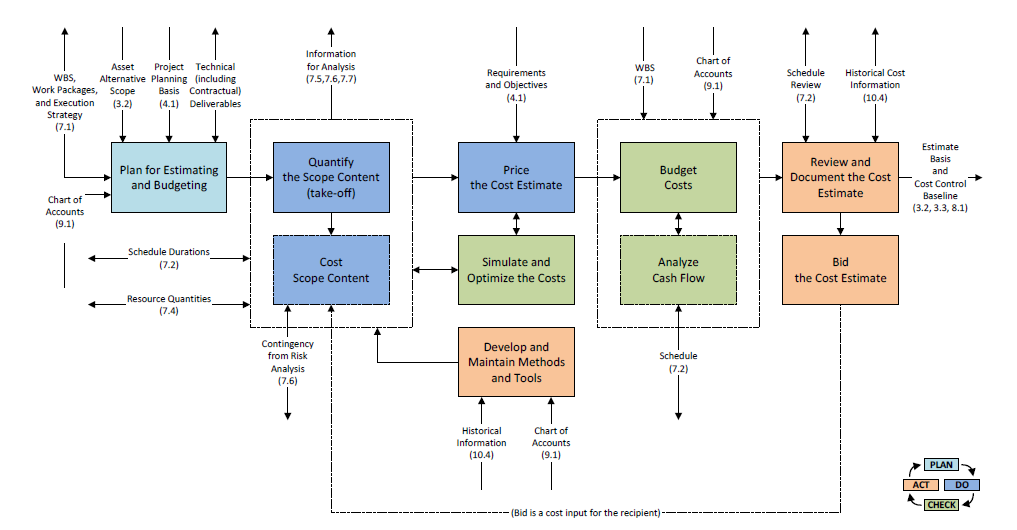

Guild of Project Controls suggest the following process map

GAO suggest the following Cost Estimating Process

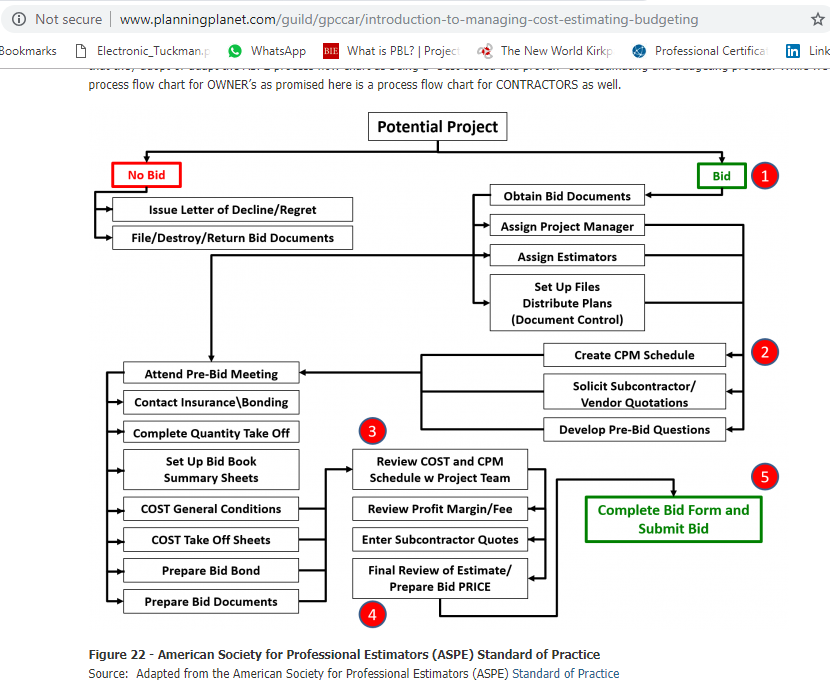

ASPE suggest the following Process Map:

Project Management Institute: Project Management Body of Knowledge – Project Cost Management

4) Step 4- Selection of the acceptable criteria.

We will compare processes if they have the following characteristics:

- Similar description

- Similar outputs

In case it is necessary, we will group processes that combined produce a very similar output.

5) Step 5- Compare the outcomes from each alternative analysis done in Step 3 against the minimum acceptable criteria from Step 4.

We have made a table to compare Processes between each other that meet acceptable criteria. We have added a column to show the outputs expected in each process. A red line represents the end of an expected process.

Colours represent the following:

Green: The process or group of processes produce the output on the first column.

Yellow: The process produces the output, not as an independent process but a subprocess. It happens that the outcome is produced by another process not included in this process map.

Red: The outcome is not produced at all by any process.

Colours represent the following:

Green: The process or group of processes produce the output on the first column.

Yellow: The process produces the output, not as an independent process but a subprocess. It happens that the outcome is produced by another process not included in this process map.

Red: The outcome is not produced at all by any process.

Notes

1. TCM

1.1 “Validation” happens during “Review and Document Estimate” process.

1.2 “Baseline” happens during “Budget Costs” process.

1.3 “Approval” happens during Project Implementation Process, during the “Authorize and Accept Project” process.

2. GPC:

2.1 “Budget” happens in the process 08.4.3.10 Budget, Authorization or Control (GPC Level 3 Cost Estimate), 08.6.3.2 Contractor Cost Baseline, Bid or Tender - (GPC Level 5 Cost Estimate) and 08.10.3.1 Communicate the Cost Estimate / Cost Budget

2.2 “Cash Flows” happens in process “09.3.3.2.3 Reviewing Both Owner and Contractor Cash Flows” which is a process included in “Measuring Capturing Progress Updating the Schedule” Module. This process is not include it in the Process Map shown.

2.3 "Approval" happens in process “Define Top Down Cost Estimate (Owner)” in the sub process 08.4.3.10 Budget, Authorization or Control (GPC Level 3 Cost Estimate) for the OWNER and in the process “Developing Bottom Up Cost Estimate (Contractor)” as an output for the CONTRACTOR.

2.4 “Tendering” happens during 08.6.3.3 What is Activity Based Costing with a note that it also appears in 05.4.3.6 Contractors Cost Estimating, Budgeting and Bidding Process

3. GAO:

3.1 GAO’s process “Develop point estimate and compare it to an independent cost estimate” was split in two, “Develop Point Estimate” and “Compare it to an independent cost estimate”. So, it can be equivalent to validation processes of GPC.

3.2 “Budget” and “Analyze Cash Flow” happen during “Develop Point Estimate” process.

3.3 “Tendering” is not mentioned in GAO’s guide.

4. ASPE:

4.1 It does not show any process after finishing Cost Estimate and Quantity take-off. The author does not have the standard of ASPE to research if any other documents are outcomes of other processes.

4.2 “Tendering” can be included in the process of “Set up Bid Book Summary Sheets”.

5. PMI:

5.1 “Validation” happens during “Estimate Cost” process. The process includes a Decision Making technique to vote for the best outcome.

5.2 “Risk Analysis” happens during “Estimate Cost” process. As shown in the flow, the Risk Register is updated as an output of the process.

5.3 “Analyze Cash Flow” happens during “Develop Schedule” process. The output “Schedule Data” contains information about cashflow projections.

5.4 “Documentation” happens as a result of “Estimate Costs”. The Basis of Estimate is a result as part of Project Documents.

5.5 “Baseline” happens as a result of “Determine Budget” process.

5.6 “Approval” happens during “Determine Budget” process.

5.7 “Tendering” is not mentioned at all as a result of the Cost Management Process. It is only mentioned as an output for the Procurement Management Process to request proposals.6) Step 6- Selection of the “best”.

As shown in the table above, GPC and GAO have continuity in their processes until to deliver an “assessment of the estimate”. These two are better than TCM which do not have a validation or revision of the estimate before simulation. TCM does the review at the moment of documentation of the estimate, after few processes later and a preliminary revision or validation could be good to find out errors or missing data in the estimate.

Then we can notice that GAO and GPC do not show any process for budgeting or cashflow but as explained in the previous step, those processes are included in other processes. Perhaps, a better process map can show all the processes are considered to prepare an optimum estimate

7) Step 7- How to plan on tracking/reporting on recommended choice.

The next step is to determine what the attributes are to determine what a good process for estimating and budgeting is.

The next step is to determine what the attributes are to determine what a good process for estimating and budgeting is.

8) REFERENCES.

1. Guild of Project Controls. (2015, October 03). 08.01 Introduction to Managing Cost Estimating Budgeting Rev 1.03. Retrieved September 15, 2018, from http://www.planningplanet.com/guild/gpccar/introduction-to-managing-cost-estimating-budgeting

2. Guild of Project Controls. (2015, October 03). 08-4 Creating_the_owners_cost_estimate_top_down_-_rev_1.02. Retrieved September 15, 2018, from http://www.planningplanet.com/guild/gpccar/creating-the-owners-cost-estimate

3. Guild of Project Controls. (2015, October 03). 08-6_developing_the_contractors_cost_estimate_bottom_up_-_rev_1.01. Retrieved September 15, 2018, from http://www.planningplanet.com/guild/gpccar/developing-the-contractors-cost-estimate-bottom-up

4. Guild of Project Controls. (2015, October 03). 09-3_measuriing__capturing_progress__updating_the_schedule_-_rev_1.03. Retrieved September 15, 2018, from http://www.planningplanet.com/guild/gpccar/capturing-progress-updating-schedule

5. H. Lance Stephenson. (2015). Total cost management framework: An Integrated Approach to Portfolio, Program, and Project Management (2nd ed.). Morgantown, WV: AACE International. Page 176 - 183

6. GAO Cost Estimating and Assessment Guide- Best Practices for Developing and Managing Capital Program Costs. Page 8.

7. A Guide to the Project Management Body of Knowledge (PMBOK® Guide), 6th ed. Newton Square, Pa: Project Management Institute, Inc. 2017. Page 231- 270

1. Guild of Project Controls. (2015, October 03). 08.01 Introduction to Managing Cost Estimating Budgeting Rev 1.03. Retrieved September 15, 2018, from http://www.planningplanet.com/guild/gpccar/introduction-to-managing-cost-estimating-budgeting

2. Guild of Project Controls. (2015, October 03). 08-4 Creating_the_owners_cost_estimate_top_down_-_rev_1.02. Retrieved September 15, 2018, from http://www.planningplanet.com/guild/gpccar/creating-the-owners-cost-estimate

3. Guild of Project Controls. (2015, October 03). 08-6_developing_the_contractors_cost_estimate_bottom_up_-_rev_1.01. Retrieved September 15, 2018, from http://www.planningplanet.com/guild/gpccar/developing-the-contractors-cost-estimate-bottom-up

4. Guild of Project Controls. (2015, October 03). 09-3_measuriing__capturing_progress__updating_the_schedule_-_rev_1.03. Retrieved September 15, 2018, from http://www.planningplanet.com/guild/gpccar/capturing-progress-updating-schedule

5. H. Lance Stephenson. (2015). Total cost management framework: An Integrated Approach to Portfolio, Program, and Project Management (2nd ed.). Morgantown, WV: AACE International. Page 176 - 183

6. GAO Cost Estimating and Assessment Guide- Best Practices for Developing and Managing Capital Program Costs. Page 8.

7. A Guide to the Project Management Body of Knowledge (PMBOK® Guide), 6th ed. Newton Square, Pa: Project Management Institute, Inc. 2017. Page 231- 270